This year marks the first year applicable large employers (ALE; 50+ full time or full-time equivalent employees) are required to report employer-sponsored healthcare coverage to the IRS and provide statements to full-time employees under IRS Sections 6055 and 6056. To help circumvent common misperceptions and errors, this two-part blog series will look at: 1) what needs to be reported, what forms need to be used, and who needs to comply with reporting requirements; and 2) methods of reporting, deadlines, and penalty relief.

What needs to be reported?

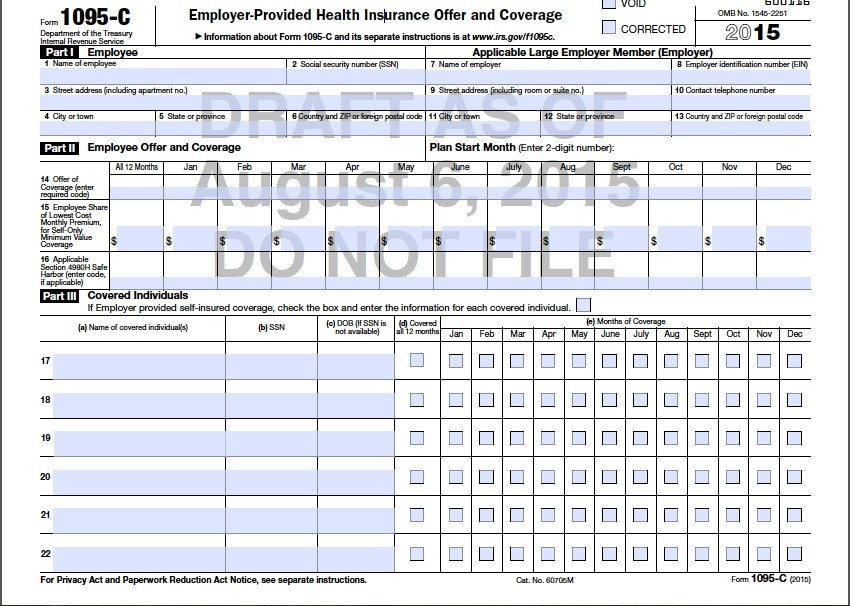

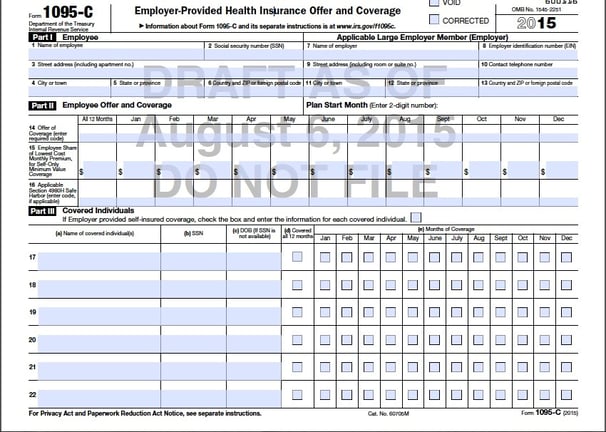

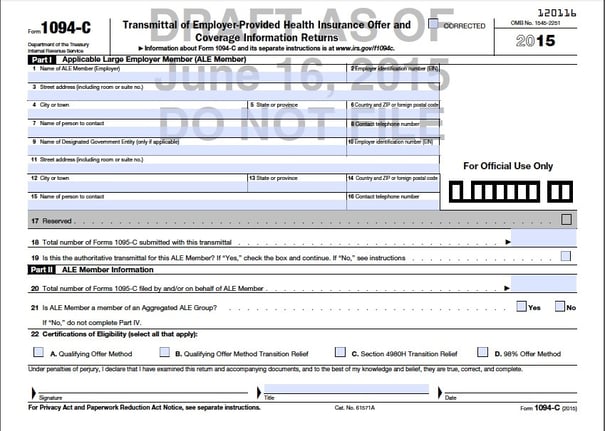

All ALEs are required to report on health coverage offerings for all full-time employees (by month), regardless of if coverage was offered and/or accepted by none, some or all employees using Form 1095-C*, Employer-Provided Health Insurance Offer and Coverage and Form 1094-C*, Transmittal of Employer-Provided Health Insurance Offer and Coverage Information Returns. In addition, ALEs are required to provide a statement to each full-time employee with the same information reported to the IRS using Form 1095-C*, which helps employees determine if they qualify for the premium tax credit.

The IRS has published a quick guide for these two forms, detailing the information needed for both. For ALEs that self-insure, section III of Form 1095-C* needs to be filled out; for employers who offer fully insured coverage, section III can be left blank.

Who is expected to report?

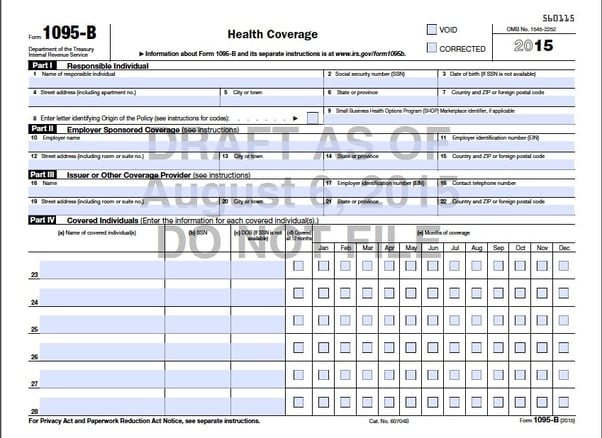

No matter if you are fully insured through a carrier or self-insure group coverage, all ALEs are expected to provide information to the IRS. This includes for-profit, nonprofit, and government organizations. If an organization is part of an aggregated group that qualifies as an ALE, each company is required to file their own forms for all full-time employees using its individual employer identification number (EIN), regardless of if the individual organization has 50+ full-time employees or not. Organizations who do not qualify as an ALE but do provide self-insured coverage are required to report to the IRS and provide employee statements (using Form 1095-B and Form 1094-B) even though they are not subject to the employer shared responsibility provisions.

For more information about ACA reporting requirements, check out our webinar on September 29th or contact Nonstop directly.

* Please note these forms are current DRAFT documents. The IRS has not released final documents for Forms 1095-C, 1094-C, 1095-B, or 1094-B.

IRS Form 1095-C*

IRS Form 1094-C* (page 1)

IRS Form 1095-B*

IRS Form 1094-B*

Want to join Nonstop and reporting expert Rachel Johnson to learn more about these new forms?

Sign up for our webinar on September 29th, 2015:

The information and materials herein are provided for general information purposes only and are not intended to constitute legal or other advice or opinions on any specific matters and are not intended to replace the advice of a qualified attorney, plan provider or other professional advisor. This information has been taken from sources believed to be reliable, but there is no guarantee as to its accuracy. This communication does not constitute a legal opinion and should not be relied upon for any purpose other than its intended educational purpose.